07-12-2019 |

S corporations, also called “S Corps”, are the largest tax filing entity in the United States. Nonetheless, I find that entrepreneurs are sometimes confused about what an S Corp is and why they should consider one. My goal with this post is to clear up misconceptions about S Corps and provide some insight as to the advantages and tax planning strategies an S Corp entity structure might provide you.

Contrary to what you might infer (and what would otherwise make perfect sense), S Corps are not necessarily corporations. Generally, any type of entity, including limited liability companies (“LLCs”), partnerships, and corporations, may elect to be an S Corp. This is because the “S” in S Corp refers to Subchapter “S” of the Internal Revenue Code, which is the law providing the means for the federal government to assess and collect taxes (the “Code”). When any entity elects to become an “S Corp”, it elects to be taxed under a different Subchapter of the Code than it normally would: Subchapter S. For this reason, an S Corp may alternatively and perhaps less confusingly be referred to as a “Subchapter S entity”.

A Subchapter S entity is a federal tax hybrid. On one hand, it resembles an LLC or a partnership, as there is so-called “pass-through” taxation. Pass-through taxation means that the entity’s profits and losses flow through to, and are reported on, the personal tax returns of its owners (via a form called Schedule K-1). The entity itself has an annual tax return but does not pay taxes. Taxes are paid by the owners at their personal income tax rates according to each owner’s allocation of the entity’s profits (if any). This means Subchapter S entities are immune from the “double taxation” dilemma confronting traditional corporations (so-called “C” corporations), which arises from the multiple layers of tax levied on: (a) a corporation’s profits, and (b) the money or property a corporation actually distributes to its shareholders (i.e., its dividends).

On the other hand, Subchapter S entities differ significantly from other pass-through entities. First, because Subchapter S was designed with small businesses in mind, an entity making an S election may only have 100 shareholders and one class of stock. Additionally, only eligible shareholders (e.g., individuals, decedents’ estates, certain prescribed trusts, but not nonresident aliens) may be owners of a Subchapter S entity. With regard to taxation, a Subchapter S entity’s income and distributions may not be specially allocated like that of a partnership or LLC. Generally, any income or loss must be allocated to shareholders of the Subchapter S entity on a per-share, per-day basis. An illustration of how this works follows:

Company S (“S”), a corporation with a Subchapter S election, has 1,000 outstanding shares of stock. A owns 500 of the shares; B owns the other 500 shares. S earns $360,000 of income in the first half of Year 1. In the second half of Year 1, S earns only $5,000.

What amount of income will A report on his personal tax return for Year 1?

- $365,000 (annual income) / 365 (days per year) = $1,000 per day.

- $1,000 (per day) / 1,000 (outstanding shares) = $1.00 per share per day.

- $1.00 (per share per day) x 500 (# A’s shares) x 365 days (# days A held shares) = $182,500 = A’s allocation of S’s income in Year 1.

What if B sold his shares during the middle of Year 1 to C?

- $1 (per share per day) x 500 (# B’s shares) x 182.5 (# days B held shares) = $91,250 = B’s pro rata share of S’s income in Year 1.

- $1 (per share per day) x 500 (# C’s shares) x 182.5 (# days C held shares) = $91,250 = C’s pro rata share of S’s income in Year 1.

Note that despite the fact that S earned only $5,000 in the period that C owned his shares, because of the strict allocation rules applicable to Subchapter S entities, C must pay taxes on $91,250. The Code has a tool for avoiding this inequitable result. Upon such a transfer, all owners of a Subchapter S entity can consent to a so-called “closing of the books” election under Sec. 1377(a)(2) of the Code. This is explained in the following example.

What if B sells his shares to C in the middle of Year 1 and A, B, and C agree to make a “closing of the books” election under Sec. 1377(a)(2)?

- A’s pro-rata income allocation remains the same = $182,500.

- B’s pro rata income allocation is now calculated as follows:

- $360,000 (income during period B owned shares) / 182.5 (# days B owned shares) = $1972.60 per day.

- $1972.60 (per day) / 1,000 (outstanding shares) = $1.9726 per share per day.

- $1.9726 (per share per day) x 500 (# B’s shares) x 182.5 (# days B owned shares) = $179,999.75 allocated income to B.

- C’s pro-rata income allocation is now calculated as follows:

- $5,000 (income during period C owned shares) / 182.5 (# days C owned shares) = $27.40 per day.

- $27.40 (per day) / 1,000 (outstanding shares) = $.0274 per share per day.

- $0.0274 (per share per day) x 500 (# C’s shares) x 182.5 (# days C owned shares) = $2,500.25 allocated income to C.

As you can see, except where a closing of the books election is made, the strict income allocation rules applicable to a Subchapter S entity make it more difficult to strategically and creatively allocate income, which is otherwise possible in other pass-through entities. While the above examples speak only to income allocation for tax purposes, distributions of money or property to Subchapter S entity owners must also be made according to similar allocation rules. This is the primary obstacle business owners create for themselves by making a Subchapter S election. Additionally, owners of C corporations desiring to make an S election face a Built-In Gains (“BIG”) tax on any appreciated assets of the corporation, meaning that they particularly should tactfully consider whether an S election is in their best interests.

Nonetheless, the tax planning strategies available under Subchapter S make the election worthwhile, depending on the circumstances.

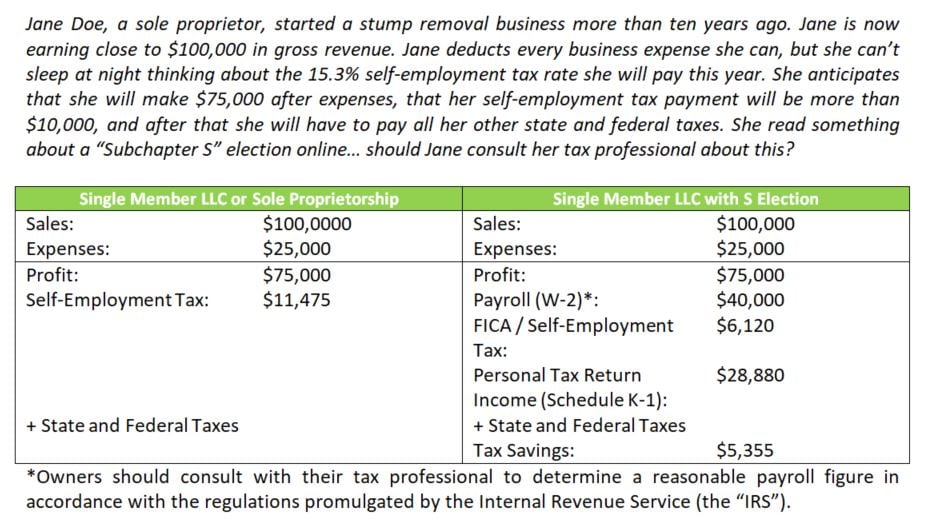

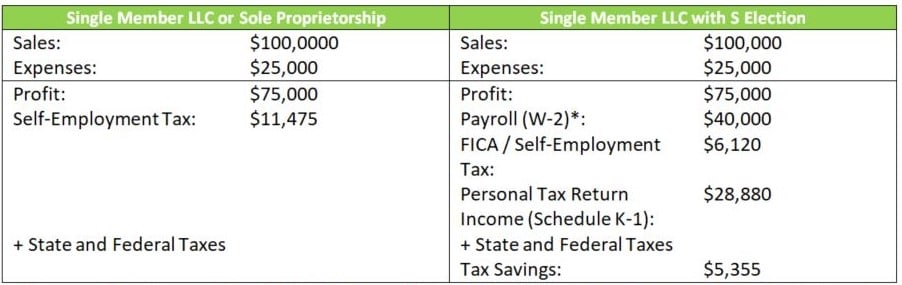

Notably, Subchapter S entity owners can save immensely on self-employment taxes. Currently, the self-employment tax rate is 15.3% (consisting of 12.4% for Social Security; 2.9% for Medicare). Subject to a few rare exceptions, owners of pass-through entities must pay this rate on the first $128,400 of their income (a 2018 figure subject to adjustment). However, under Subchapter S, business owners may take a reasonable payroll (i.e., salary) for the services they provide the business through a W-2. Then, the Subchapter S entity’s income that is not directly attributable to the W-2 salary may be treated as distribution income instead of self-employment income. This distribution income will not be subject to the self-employment tax.

Thus, with a Subchapter S entity, owners pay self-employment tax on their payroll, not on distributions made from the profit of the Subchapter S entity. Below is a basic example illustrating this concept. Please keep in mind that this example is oversimplified for demonstrative purposes (i.e., it does not take into account the above-the-line deduction available for half of the self-employment tax attributable to the business).

Jane Doe, a sole proprietor, started a stump removal business more than ten years ago. Jane is now earning close to $100,000 in gross revenue. Jane deducts every business expense she can, but she can’t sleep at night thinking about the 15.3% self-employment tax rate she will pay this year. She anticipates that she will make $75,000 after expenses, that her self-employment tax payment will be more than $10,000, and after that, she will have to pay all her other state and federal taxes. She read something about a “Subchapter S” election online… should Jane consult her tax professional about this?

*Owners should consult with their tax professional to determine a reasonable payroll figure in accordance with the regulations promulgated by the Internal Revenue Service (the “IRS”).

In the example above, it would be advantageous for Jane Doe to make an S election for her business. From the self-employment tax planning associated with an S election, she could save substantially on her taxes paid each year. However, possible savings on self-employment tax is only one benefit of the Subchapter S entity. There are also many other strategic advantages to making an S election, some of which include:

- Owners of Subchapter S entities may be entitled to the 20% deduction for Qualified Business Income under Section 199A of the Code enacted as part of the 2017 Tax Cuts and Jobs Act (a significant deduction you should be aware of and consult your tax professional about).

- Subchapter S entity losses are deductible on the personal tax returns of the owners to the extent the owners have basis in the Subchapter S entity’s equity. With a traditional C corporation, losses are trapped inside the corporation.

- A Subchapter S entity can pass through certain items of income without re-characterization, meaning that Subchapter S entity’s charitable contributions are not subject to the 10% limitation imposed on C corporations.

- Subchapter S entities are generally not subject to Personal Holding Company Tax or Accumulated Earnings Tax.

- Subchapter S entities can immediately create capital gains so a taxpayer will not be forced to carry forward, and can instead offset, capital losses subject to limited deductibility (i.e., $3,000 per year).

Hopefully, this article has clarified for you the definition of an S Corp and provided you a glimpse into the tax planning advantages a Subchapter S election might provide you. Overall, I am a firm believer that the S election is a viable option for small business owners, so long as the election aligns with the owners’ financial situation, goals, and business strategy. As long as the Code and its corresponding regulations are closely followed, business owners can often achieve a lower effective tax rate with an S election.

Please note, however, that any tax strategy described in this article must be implemented in strict accordance with the Code and the regulations promulgated by the IRS. Before implementing any such strategies, it is strongly recommended that you consult your tax lawyer or other tax/accounting professional. This post is for informative purposes only and should not be relied on as tax advice.

In the event you have any further questions about entity selection and whether a Subchapter S election is right for your business, please do not hesitate to call an attorney with BrownWinick’s Business and Corporate Law practice group today.

Meet the Author: